Why Real Money Control Begins With Everyday Awareness

Most people don’t believe they’re “terrible with money.”

They feel outpaced.

Outpaced by bills.

Outpaced by savings goals.

Outpaced by the version of life they thought they’d already be living.

That distance — between what you plan and what actually happens — is where financial tension settles in.

We’re usually told the fix is more discipline.

Tighter rules.

Stronger willpower.

But money rarely responds to pressure.

What’s usually missing isn’t discipline.

It’s dexterity.

What does “financial dexterity” really point to?

The word dexterity traces back to the Latin dexter, meaning right-handed or skillful.

In much older English, there was even a term — “dext” — referring to the right side, the capable hand, the side that knows its way.

It’s not a word anyone uses now.

But the concept behind it still carries weight.

Financial dexterity isn’t about flawless money habits.

It’s about being able with money.

Able to:

- Understand where your money ends up

- Make adjustments without spiraling

- Respond rather than shut down

- Stay engaged instead of guessing

That’s the line between people who feel steady with money and those who feel constantly off-balance.

And it’s exactly where most budgeting advice loses people.

Budgeting isn’t broken. Disconnection is.

Most budgeting tools are built on a hopeful assumption.

They assume people:

- Record every purchase

- Categorize perfectly

- Review charts weekly

- Enjoy financial admin

That’s not how life works.

Real life looks more like:

- Receipts stuffed in bags

- Charges that don’t ring a bell

- “I’ll look at that later”

- A slight knot in your stomach when opening your bank app

The problem isn’t a lack of care.

It’s that money systems feel detached from real behavior.

When money feels theoretical, people check out.

When it feels immediate, people adjust.

That’s where awareness starts to shift things.

Expense tracking isn’t about cutting yourself off

A lot of people carry the same worry.

“If I track my spending, I’ll just end up feeling guilty.”

But avoiding visibility doesn’t reduce pressure.

It just delays the moment it shows up.

Tracking expenses — especially in a simple, receipt-first way — does something else entirely:

It reframes money as information, not judgment.

You stop asking:

“What’s wrong with me?”

And start asking:

“What actually happened here?”

That single shift lowers stress.

And it builds financial dexterity — the calm confidence that comes from clarity, not control.

Why money systems don’t work for most Americans

The US sits high on the list for financial stress.

Not only because living costs keep climbing —

but because many financial tools feel designed for a different kind of person.

Someone hyper-organized.

Someone disciplined by default.

Someone with time to spare.

Most people don’t want layered dashboards.

They want understanding.

They want to know:

- What did I spend today?

- Where did it go?

- Am I more or less okay?

That’s it.

When tools answer those questions, behavior shifts without force.

Control usually comes after the purchase

Most financial advice tries to stop spending before it happens.

But spending itself isn’t the issue.

Disconnection is.

You don’t need to quit coffee.

You need to notice the pattern.

You don’t need to remove enjoyment.

You need to see what’s quietly draining your sense of ease.

That’s why expense logging — capturing spending after it happens — works better than pre-set limits.

It ties money to real moments, not delayed self-criticism.

That’s financial dexterity at work.

Why “always-on tracking” often pushes people away

Many apps sell real-time tracking as the solution.

In reality, it often:

- Feels intrusive

- Heightens anxiety

- Strips away context

- Encourages avoidance

Money isn’t just math.

It’s emotional.

When people feel monitored, they retreat.

When they feel informed, they participate.

That’s why post-spend awareness — logging receipts and reviewing expenses afterward — tends to stick.

It matches how people actually live.

Receipts tell the story bank feeds miss

Bank transactions are vague.

A receipt shows:

- What you bought

- Why it made sense at the time

- The situation surrounding the purchase

That context changes everything.

It’s the difference between:

- “$47.80 – Unknown Vendor”

- “Groceries after a late workday”

One triggers self-judgment.

The other builds understanding.

Understanding leads to flexibility.

Flexibility builds confidence.

Confidence leads to better choices.

Financial confidence is quiet

People often picture confidence as:

- Large balances

- Perfectly balanced budgets

- Zero impulse buys

In practice, it’s much subtler.

It looks like:

- Staying calm when numbers shift

- Knowing where to adjust

- Feeling capable instead of overwhelmed

That’s dexterity again.

Not control.

Not restriction.

Just skill.

Awareness beats ambition

Most people start with big intentions.

“I’m saving ten grand.”

“I’m cutting eating out.”

“I’m getting serious.”

Those goals aren’t wrong.

They’re just disconnected from daily behavior.

Smaller awareness habits work better:

- Logging receipts once a day

- Checking weekly totals

- Noticing trends without fixing them immediately

This creates movement without pressure.

And movement is what actually changes habits.

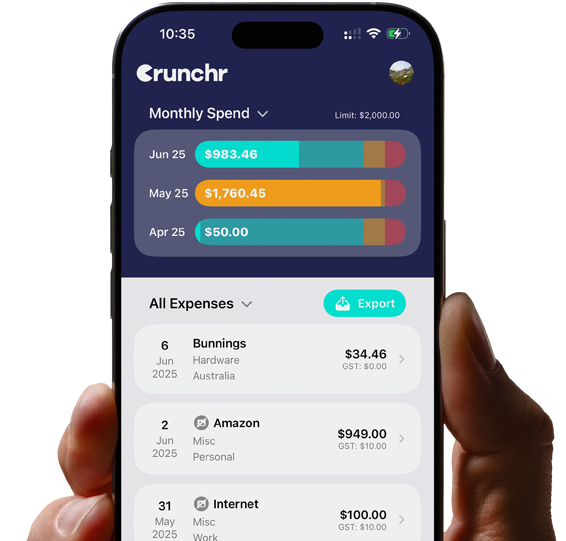

Why Crunchr is built around expense logging

Crunchr isn’t designed to hover over your money.

It’s designed to meet money where it actually shows up.

After the spend.

With context.

Without judgment.

This approach:

- Lowers anxiety

- Improves consistency

- Builds trust in your own patterns

You don’t need to be “good with money” to begin.

You just need to be willing to look.

That’s enough.

Financial dexterity develops gradually

No one becomes capable overnight.

Dexterity — whether physical or financial — comes from repetition without punishment.

You log expenses.

You notice patterns.

You adjust organically.

Not because someone told you to.

But because the picture became clearer.

That’s how lasting financial change happens.

Quietly.

Over time.

Without force.

Money isn’t moral. It’s feedback.

One of the most damaging ideas people carry is that money reflects who they are.

It doesn’t.

Spending isn’t failure.

Saving isn’t virtue.

Money is information.

When you treat it that way, tension eases and clarity grows.

And clarity is what most people are actually searching for when they download a budgeting app.

A right-hand relationship with money

If we come back to that old word — dext — it points to something simple.

A “right-hand” relationship with money isn’t about dominance.

It’s about familiarity.

You don’t overthink your dominant hand.

You trust it.

That’s what financial dexterity feels like.

Not obsession.

Not avoidance.

Just ease.

Final thought

You don’t need to reinvent your life to feel steadier with money.

You don’t need extreme rules or rigid systems.

You need:

- Visibility

- Context

- Tools that respect real human behavior

That’s how everyday Americans build real confidence with money.

One receipt.

One moment of clarity.

One small shift at a time.